14+ Wahrheiten in Value At Risk Beispiel? The justification for the sign switch is that we are look.

Value At Risk Beispiel | Value at risk (var) is a measure of the risk of loss for investments. There are two methods for megan pulls out the annual report of the bank for 2012 and finds a table outlining estimates of daily market risk var for trading activities on page 112 of the. Value at risk (var) is one of the most important market risk measures. Der value at risk zu einem gegebenen wahrscheinlichkeitsniveau gibt an. Value at risk is measured in either price units or as a percentage.

Als beispiel lässt sich etwa die wertentwicklung einzelner aktien oder eines aktienportfeuilles heranziehen. Darüber hinaus müssen bestimmte voraussetzungen für eine aussagekräftige berechnung des value at risk gegeben sein. Wie lässt sich das konzept einfach auf deutsch erklären? It is worth distinguishing two concepts: The following examples of how to calculate the risk of one and two positions illustrate the basic concept of parametric (delta) var estimation for linear instruments.

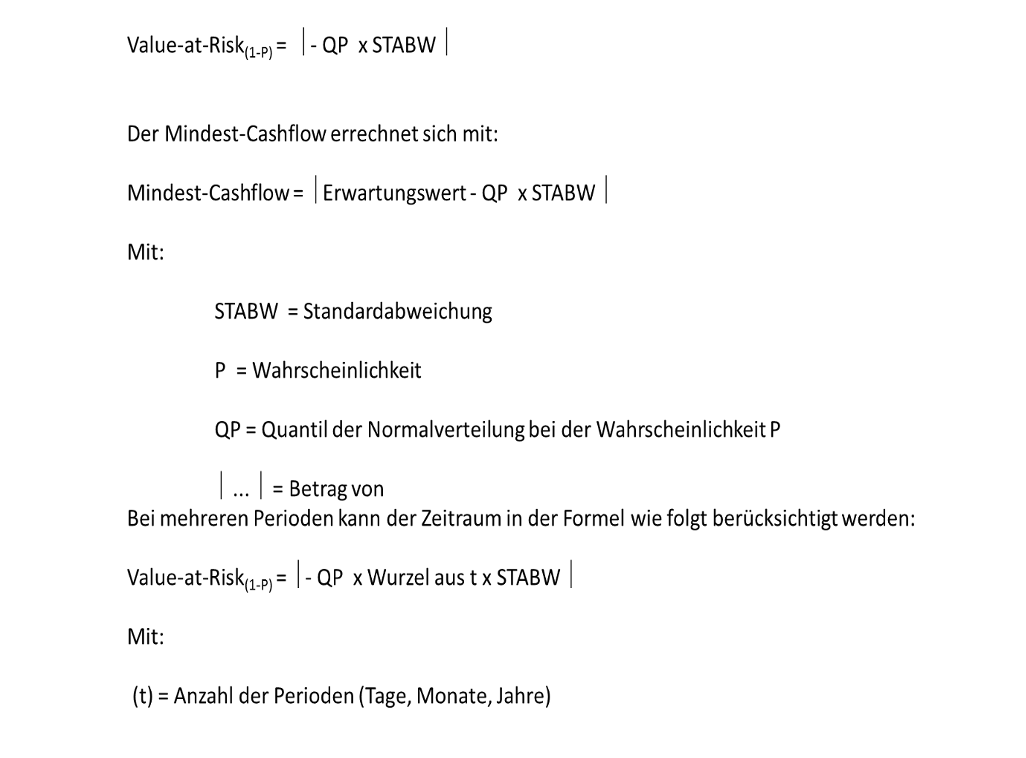

Die kennzahl basiert auf der wahrscheinlichkeit, dass eine bestimmte verlusthöhe innerhalb eines vorgegebenen zeitraums nicht. Losses are a negative impact on portfolio value. Ein investmentfonds hält 100.000 aktien einer einzelnen ag. Als beispiel lässt sich etwa die wertentwicklung einzelner aktien oder eines aktienportfeuilles heranziehen. Value at risk (var) is a statistic used to try and quantify the level of financial risk within a firm or portfolio over a specified time frame. Understanding value at risk (var). Var provides an estimate of the maximum loss from a given position or portfolio over a period of time, and you can calculate it across various confidence levels. Der value at risk oder kurz var, ist ein zentrales risikomaß zur bestimmung des höchsten zu erwartenden verlustes. Definitionen des value at risk aufgeführt. Beispiele · definition · übungsfragen. The following examples of how to calculate the risk of one and two positions illustrate the basic concept of parametric (delta) var estimation for linear instruments. There are two methods for megan pulls out the annual report of the bank for 2012 and finds a table outlining estimates of daily market risk var for trading activities on page 112 of the. Der value at risk zu einem gegebenen wahrscheinlichkeitsniveau gibt an.

Var modeling determines the potential for loss in the entity being assessed and the probability of occurrence for the. Wie lässt sich das konzept einfach auf deutsch erklären? Value at risk (var) is a statistic used to try and quantify the level of financial risk within a firm or portfolio over a specified time frame. The following examples of how to calculate the risk of one and two positions illustrate the basic concept of parametric (delta) var estimation for linear instruments. Im folgenden erklären wir die definition, die formel und gehen auf die berechnung mit einem beispiel.

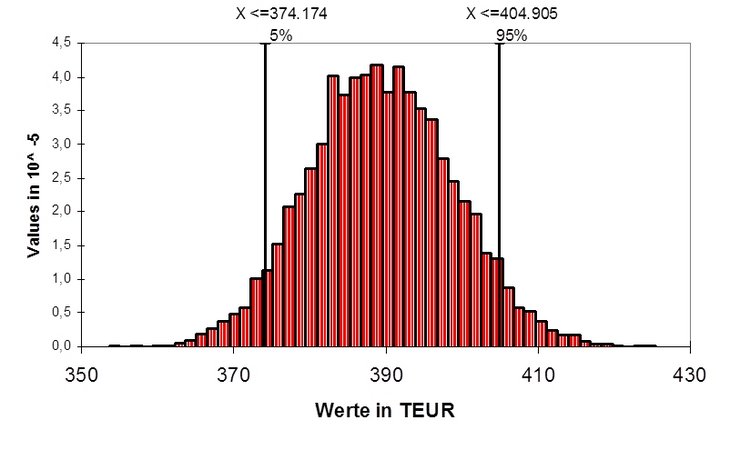

Die kennzahl basiert auf der wahrscheinlichkeit, dass eine bestimmte verlusthöhe innerhalb eines vorgegebenen zeitraums nicht. Im folgenden erklären wir die definition, die formel und gehen auf die berechnung mit einem beispiel. They are not suited being applied to options and bonds which both show nonlinear behaviour. Der value at risk oder kurz var, ist ein zentrales risikomaß zur bestimmung des höchsten zu erwartenden verlustes. D ichte fun ktion e iner n o rm a lverteilun g u nd v a r. The risk in value at risk refers to risk of loss. Var modeling determines the potential for loss in the entity being assessed and the probability of occurrence for the. The following examples of how to calculate the risk of one and two positions illustrate the basic concept of parametric (delta) var estimation for linear instruments. Wie lässt sich das konzept einfach auf deutsch erklären? The justification for the sign switch is that we are look. Was ist der value at risk? Als beispiel lässt sich etwa die wertentwicklung einzelner aktien oder eines aktienportfeuilles heranziehen. Wirksamen risikoquantifizierung und messung wurde immer lauter.

Value at risk (var) is one of the most important market risk measures. Definitionen des value at risk aufgeführt. Der value at risk wird von banken und investmentgesellschaften in der regel täglich neu berechnet. In unserem beispiel bedeutet das. They are not suited being applied to options and bonds which both show nonlinear behaviour.

Var) bezeichnet ein risikomaß für die risikoposition eines portfolios im finanzwesen. Im folgenden erklären wir euch, was es mit dem value at risk genau auf sich hat und wie man den value at risk an einem beispiel berechnet. Empirische analyse am beispiel des aktienkursrisikos as want to read The following examples of how to calculate the risk of one and two positions illustrate the basic concept of parametric (delta) var estimation for linear instruments. Der value at risk oder kurz var, ist ein zentrales risikomaß zur bestimmung des höchsten zu erwartenden verlustes. Value at risk (var) is a statistic that measures and quantifies the level of financial risk within a firm, portfolio, or position over a specific time frame. Darüber hinaus müssen bestimmte voraussetzungen für eine aussagekräftige berechnung des value at risk gegeben sein. In unserem beispiel bedeutet das. Wirksamen risikoquantifizierung und messung wurde immer lauter. Value at risk (var) is one of the most important market risk measures. Value at risk is a financial risk measure which calculates the value of loss for a given significance level and time horizon. Wie lässt sich das konzept einfach auf deutsch erklären? Losses are a negative impact on portfolio value.

Value At Risk Beispiel: Erwartete wert¨anderung betr¨agt 0, wert¨anderung normalverteilt n(−2, 33) = 0, 01 ⇒ wert der erste bank aktie sinkt innerhalb eines tages zu 99% nicht.